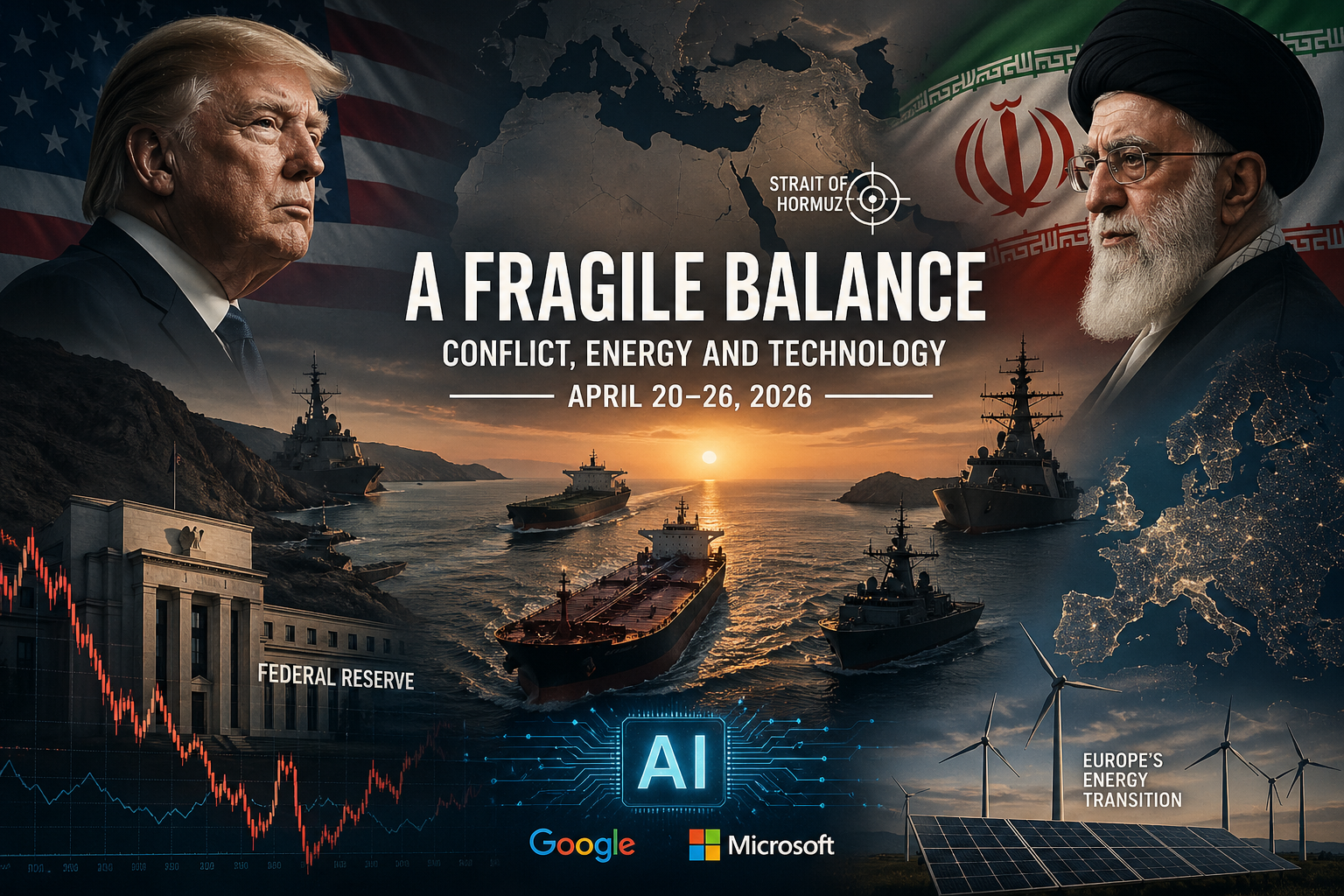

A fragile balance: energy, conflict and technology in the week of April 20–26, 2026

The week of April 20–26, 2026 was not defined by stability, but by controlled tension. The conflict between the United States and Iran did not fully escalate, yet it did not stabilize either. On April 21, the administration led by Donald Trump decided to extend the ceasefire, delaying a direct strike and allowing Iran time to present a potential diplomatic proposal. The decision came after several days of mounting pressure, including direct threats targeting Iran’s energy infrastructure if no agreement was reached.

At the same time, the situation in the Strait of Hormuz became the focal point of global tension. The United States maintained its naval blockade, intercepting commercial vessels and controlling access to Iranian ports, while Iran responded by restricting maritime passage and seizing ships in the region. This was no longer a theoretical risk, but a series of concrete actions, ship interceptions, attacks on transport routes, and military control over one of the world’s most critical energy corridors.

The implications were immediate. Oil prices surged above key thresholds as markets reacted to uncertainty in supply flows. Europe, heavily dependent on imported energy, stands among the most exposed regions. The aviation sector in particular faces direct pressure, as jet fuel, derived from crude oil, becomes more expensive and potentially harder to secure, raising the risk of reduced operations and higher costs. In contrast, the United States remains in a more resilient position, supported by strong domestic energy production and lower reliance on this specific route, giving it a strategic advantage in a prolonged crisis scenario.

Meanwhile, tensions were not confined to the external stage. Toward the end of the week, an armed incident targeting Donald Trump highlighted how geopolitical pressure can spill into domestic instability. Although the situation was quickly contained, it underscored how leadership figures become focal points of tension during periods of heightened global uncertainty.

From an economic perspective, the message delivered by the Federal Reserve was clear, interest rates are not expected to decline in the near term. Markets reacted with volatility, as the cost of capital remains elevated, affecting company valuations and slowing investment activity. The global economy now sits in an intermediate phase, where inflation is not fully under control, yet growth is not strong enough to justify monetary easing.

At the same time, Europe is accelerating its transition toward renewable energy, not only as a climate objective but as a direct response to geopolitical risk. The situation around Hormuz has exposed the vulnerability of traditional energy routes, turning investments in solar and wind into a strategic necessity rather than a policy preference. In this context, crises do not slow down transitions, they accelerate them.

On another level, but equally significant, this week reinforced a major technological shift. Companies such as Google and Microsoft continue to integrate artificial intelligence directly into their core products, from search engines and office tools to cloud infrastructure. There was no single breakthrough announcement, but rather a consolidation of direction, AI is no longer a standalone product, but an embedded layer in how people work and make decisions. This shift is redefining competition, moving it away from physical resources toward control over information and productivity.

Taken together, this week highlighted how multiple critical systems are operating under simultaneous pressure. Energy is exposed to geopolitical conflict, financial markets remain sensitive to central bank policy, and technology continues to advance faster than regulatory frameworks can adapt. This is not a full-scale crisis, but neither is it stability. It is a temporary balance, sustained by strategic decisions and calculated delays, in a world where every move carries weight.